Is ‘Extend and Pretend’ Coming to an End? Maybe Not.

In recent months, a slew of published articles shed light on the imminent commercial real estate loan maturities and the potential ramifications for the industry and the broader economy. As these loans mature, landlords have limited financing options in today’s market. Lenders are faced with the decision: Should they foreclose on an asset (mainly office properties) that they don’t want to own and operate? Or do they choose the risky path of ‘Extend and Pretend,’ which could potentially lead to a prolonged crisis?

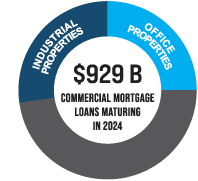

The Numbers

According to a report by the Mortgage Bankers Association, an astounding 20% ($929 billion) of the $4.7 trillion of outstanding commercial mortgages held by lenders and investors are set to mature in 2024. This is a 28% increase from the $729 billion in 2023 loan maturities. Initially, projected loan maturities for 2024 were $659 billion. However, due to a significant decline in transactions, built-in extension options, and lender and servicer flexibility, many loans scheduled to mature in 2023 were extended or otherwise modified and will now come due in 2024 or beyond.

Office loans account for 25% of the total loans maturing in 2024. While 27% of industrial property loans are also coming due, industrial continues to outperform most property types, with 124 million square feet of positive absorption from Q1 2023 to Q1 2024 and rent growth of 5.3% during that period, consistent with pre-pandemic levels.

Office Market

Of course, the most problematic loans have been in the office sector, where occupancy rates and property valuations have dropped significantly. According to a report by the National Association of Realtors (NAR), there was 58 million square feet of negative absorption from Q1 2023 to Q1 2024. Property prices fell by 7% over the past year and by 21% since their March 2022 peak, according to Green Street’s Commercial Property Price Index (CPPI). The NAR report also indicated that year-over-year, the amount of vacated office space surged by 97%, with the vacancy rate hitting a decade-high of 13.7% (up 1.1% from the prior year). Not surprisingly, San Francisco led the major metros in vacancy at 21.69%, up from 17.14% in Q1 2023. Los Angeles also made the top (actually bottom) 10, with a vacancy rate of 16.14%, up from 14.6% in 2023.

While much of the stress in the office market has been attributed to Class B and C properties, Class A properties suffered the most during that period. The withdrawal from Class A office space accounts for 49% of all vacated space, compared to the previous year, when Class B properties saw the biggest hit, with 70% of all negative absorption.

Although occupancy remains high, there are some encouraging signs for the office market. The final quarter of 2023 saw an uptick in overall leasing activity, with 37% of the year’s lease transactions completed during Q4 (renewals made up 75% of the lease transactions). The trend continued into Q1 of 2024, with national brokerages reporting increased tenant demand.

Refinancing Not an Option for Most Office Properties

The combination of high interest rates and plummeting valuations makes refinancing extraordinarily difficult for many office owners. Inflation stubbornly persists. The much-anticipated slashing of interest rates has yet to materialize, and many speculate that it may not happen at all this year. According to an article by commercial real estate finance data provider Trepp, owners who can refinance are likely to see their rates increase to 6.5%–10% on notes currently coming due, as opposed to 3%–5% before 2022. Making matters worse, Trepp reports that office properties financed by CMBS loans transferred to special servicing were found to have experienced staggering value losses — exceeding 50% in 2023.

Foreclosures Picking Up Steam

With the outlook for office space so dire, many landlords are simply surrendering their keys to the lender. REITs like Blackstone, Boston Properties, and Brookfield Properties have defaulted on mortgages and have started or completed the process of handing back the keys to office towers. Commercial real estate financial information provider ATTOM reports a significant climb in monthly commercial foreclosures since the onset of COVID-19, from a low of 141 in May 2020 to the latest tally of 625 for March 2024. More telling is the doubling of monthly foreclosures in less than a year. There were less than 300 foreclosures in May of 2023, and foreclosures have climbed steadily over the past year. In January 2024, California led the nation with 181 commercial foreclosures — a 174% increase from last year.

“This uptick signifies not just a return to pre-pandemic activity levels but also underscores the ongoing adjustments within the commercial real estate sector as it navigates through a landscape transformed by evolving business practices and consumer behaviors,” said ATTOM CEO Rob Barber in a February press release.

Extend and Pretend

Given the challenging market circumstances, many lenders are working with building owners to circumvent loan defaults through loan extensions or forbearance agreements, a practice given the tagline “Extend and Pretend” during the Great Financial Crisis (GFC). Some believe the end of the practice is coming sooner rather than later. But Ann Hambly, founder and CEO of borrower advocate firm 1st Service Solutions, doesn’t share that opinion.

Hambly says there are few options for many borrowers to refinance right now, “so in many cases (the strategy) is not to just to ‘extend and pretend’ but to ‘delay and pray’ because we’re just praying that things are better in the future than they are today.” Hambly adds that extending loans rather than foreclosing benefits lenders and special servicers because they continue to earn fees. “Everybody on the lending side is incentivized not to have this hit now,” she says. “Although we do know that things could get worse.”

And therein lies the danger of extending and pretending. The purpose of the practice is based on the idea that rates will go down (as they did following the GFC), allowing refinancing that benefits all stakeholders. There’s no guarantee that will happen, and it seems unlikely that it will happen in the near future. So, the strategy is clearly a gamble.

The Trepp article concludes with this warning: “Lenders and borrowers alike must navigate these turbulent waters with a keen understanding of the broader economic impacts, innovative financing solutions, and a strategic approach to asset management and loan extensions. The journey ahead demands a delicate balance between immediate financial pressures and long-term viability, with a clear-eyed recognition of the transformed landscape of CRE financing.”

Contact a Voit broker in your market for guidance on developing the optimal strategy for your assets.